Key Takeaways

- Superior Accuracy: AI models achieve 97%+ fraud detection accuracy, significantly outperforming legacy rules-based systems that typically plateau at 60-70%.

- Reduced False Positives: Automated behavioral analysis reduces false positives (legitimate transactions blocked) by 50-90%, maintaining a frictionless customer experience.

- Advanced Topology Mapping: Graph Neural Networks (GNNs) enable the detection of complex money laundering rings by analyzing network connections rather than isolated transactions.

- Adaptive Defense: Real-time scoring and unsupervised learning allow systems to identify and mitigate "zero-day" attacks and weaponized AI threats in milliseconds.

What is AI Fraud Detection?

AI fraud detection refers to the application of advanced machine learning algorithms—including Graph Neural Networks, unsupervised learning, and behavioral biometrics—to identify, prevent, and mitigate fraudulent financial activities in real-time. It describes how financial institutions analyze transaction patterns, device fingerprints, network topology, and behavioral signals to distinguish legitimate users from fraudsters, synthetic identities, account takeovers, and money laundering schemes while maintaining customer experience and regulatory compliance.

Quick Answer

AI fraud detection utilizes real-time machine learning to identify suspicious activity with 97% accuracy, drastically reducing financial losses and false positives by up to 90%. By replacing rigid rules with adaptive behavioral biometrics and Graph Neural Networks, financial institutions can stop sophisticated attacks like synthetic identity fraud and money laundering rings in milliseconds while ensuring legitimate customer transactions remain uninterrupted.

Quick Facts

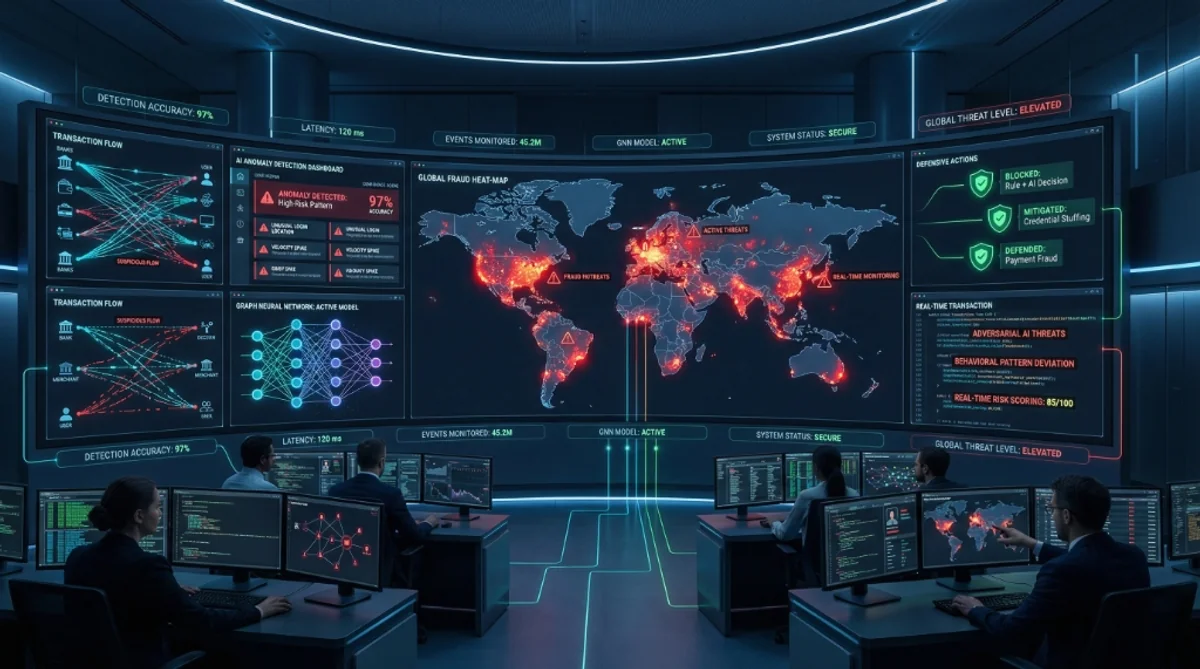

- AI Detection Accuracy: 97%+

- Rules-Based Accuracy: 60-70%

- False Positive Reduction: 50-90%

- Average Breach Cost (Finance): $6.08M (Source: IBM)

- Scoring Latency: <10ms

Key Questions This Article Answers

Why is AI better than traditional rules-based fraud detection?

AI is adaptive rather than rigid, analyzing thousands of behavioral signals including typing speed, device battery level, navigation patterns, and spending velocity to distinguish legitimate users from fraudsters. Traditional rules-based systems achieve only 60-70% accuracy and are easily bypassed by slightly modified attacks (e.g., stealing $4,999 instead of $5,000), while AI achieves 97%+ accuracy by continuously learning from new attack vectors and understanding user behavior patterns.

How does AI detect money laundering (AML) more effectively?

AI uses Graph Neural Networks (GNNs) to visualize and analyze connections between thousands of seemingly unrelated accounts, uncovering "circular" transaction patterns and complex laundering rings that linear rules miss. Money launderers break large sums into tiny, undetectable transactions ("structuring"), but GNNs can spot the laundering ring quickly by analyzing the network topology of account relationships and transaction flows.

What is the financial impact of false positives in fraud detection?

High false positive rates lead to 30% of customers switching banks after having a legitimate transaction blocked (the "insult rate"), while the average data breach costs $6.08 million for financial institutions. AI solves both problems by achieving 97%+ accuracy in detecting real fraud while reducing false positives by 50-90%, balancing security with customer experience and preventing both fraud losses and customer churn.

The New Threat Landscape: Weaponized AI

Fraudsters are no longer just teenage hackers; they are organized crime syndicates using the same AI tools we are.

1. Deepfake Voice & Video (CEO Fraud)

- The Attack: A finance director receives a call from the CFO's voice: "Transfer $500k to this vendor immediately."

- The Tech: Generative AI needs only 3 seconds of audio to clone a voice.

- The Defense: AI analysis of the audio spectrum to detect "synthetic artifacts" invisible to the human ear.

2. Generative Phishing

- The Attack: Emails that are perfectly personalized, grammatically correct, and reference specific recent transactions.

- The Tech: Using LLMs (Large Language Models) to scrape LinkedIn and craft better hooks.

- The Defense: NLP (Natural Language Processing) that analyzes the intent and context of the message, not just keywords.

3. Synthetic Identity Fraud 2.0

- The Attack: Creating a fake person who acts real for 2 years (builds credit score) before "busting out" with maxed loans.

- The Defense: Cross-Bureau linkage analysis. AI sees that "John Doe" shares a phone number with 50 other "people."

Technical Deep Dive: The AI Architectures Protecting You

Different crimes require different brains.

1. Graph Neural Networks (GNN) for AML

Money Laundering is a networking problem.

- Nodes: Bank Accounts.

- Edges: Transactions.

- The Power: GNNs don't just look at the transaction; they look at the topology.

- Example: "Account A sends to Account B." (Normal).

- Example: "Account A sends to B, who sends to C, who sends to D, who sends back to A." (Circular Detection - Laundering Signal).

- Scale: PayPal uses GNNs to analyze billions of edges in milliseconds.

2. Unsupervised Learning (Isolation Forests)

For "Zero-Day" attacks (tactics never seen before).

- Method: The AI doesn't know what fraud looks like. It only knows what normal looks like.

- Isolation: It creates a multi-dimensional map of "Normal." Any transaction that sits "far away" in the vector space is flagged.

- Result: Detecting the first wave of a new malware attack before any rules are written.

3. Recurrent Neural Networks (RNN/LSTM)

For Time-Series analysis.

- Concept: Memory.

- Application: "User X usually logs in at 9 AM. Today they logged in at 3 AM."

- Nuance: An RNN remembers that User X is traveling (seen by GPS previously), so it approves the 3 AM login. Linear rules would have blocked it.

Technical Deep Dive: 3 Lines of Defense (Application Layer)

Now that we have the brains (GNNs, etc.), how do we apply them?

1. Real-Time Transaction Scoring

Every time a card is swiped, the AI gives a risk score (0-100) in less than 10 milliseconds.

- Score less than 20: Approve.

- Score 20-80: Challenge (Send 2FA SMS).

- Score greater than 80: Decline & Alert Fraud Team.

2. Behavioral Biometrics

Passwords can be stolen. Behavior cannot. The AI analyzes:

- How you hold your phone.

- Your swiping speed.

- Mouse movement curvature. If a "login" happens with the wrong behavior, it's flagged as an Account Takeover (ATO).

3. Predictive Modeling

The AI simulates attacks against itself (Adversarial Networks) to predict how fraudsters will attack tomorrow, keeping defenses one step ahead of the Dark Web.

Real-World Impact

JPMorgan Chase: The $100M+ Savings Engine

In 2023, JPMC processed trillions in payments. The sheer volume makes manual review impossible.

- The Challenge: Business Email Compromise (BEC) and Check Fraud (still huge in the US). Rules-based systems were flagging 90% of large checks for review, creating a 3-day hold that angered clients.

- The Solution: An ensemble of 3 AI models.

- Image Analysis: Scans the physical check image for handwriting mismatches.

- Behavioral Analysis: "Does this client usually write $50,000 checks to 'Roofing Co'?"

- Network Analysis: "Is 'Roofing Co' a known shell company?"

- The Result: Reduced fraud losses by >$100M annually while clearing 99.8% of checks quickly.

HSBC: 60% False Positive Reduction with Google Cloud

HSBC monitors 400 million transactions per month.

- The Problem: The "Crying Wolf" Effect. Their legacy AML system generated thousands of alerts daily. 99% were false alarms. Analysts spent 8 hours a day clicking "Ignore."

- The Solution: They partnered with Google Cloud to build the "Dynamic Risk Assessment" (DRA). Instead of a binary "Good/Bad" flag, the AI gives a risk score.

- The Shift: Only the top 1% of risky transactions are sent to humans.

- The Result: a 60% drop in false positives. This effectively doubled the capacity of their compliance team without hiring a single new person.

PayPal: Graph Mining at Scale

PayPal loses millions to "Collusion Fraud" (Networks of fake buyers and fake sellers boosting ratings).

- The Tech: GNN (Graph Neural Networks).

- The Insight: A single fake account looks normal. But a cluster of 50 accounts all sharing the same device ID and shipping address is obvious to a Graph.

- The Result: Catching fraud rings within 3 hours of formation.

11. Global Fraud Map: Know Your Enemy

Fraud varies by geography.

| Region | Primary Threat | The AI Defense |

|---|---|---|

| North America | CNP (Card Not Present) & Check Fraud | Computer Vision (Checks) & Behavioral Biometrics. |

| Latin America (Brazil) | PIX Fraud (Instant Payment) | Real-time GNNs (Must score in < 100ms). |

| Europe (UK) | APP Fraud (Authorized Push Payment) | NLP Analysis of user intent ("Are they being coerced?"). |

| Asia (APAC) | Promo Abuse & Synthetic ID | Device Fingerprinting. |

12. The Fraud Squad 2025: New Roles

You need new talent to run these engines.

1. The Threat Hunter

- Job: proactive. They don't wait for alerts. They dive into the data lake to find patterns of fraud that the AI missed (False Negatives).

- Tool: SQL + Python.

2. The Adversarial Engineer

- Job: The "Red Team." Their job is to attack your own AI. They try to fool the model (e.g., "If I make the transaction $499 instead of $500, does it pass?").

- Goal: Find holes before the criminals do.

3. The Explainability Officer

- Job: Translating "The Neural Net said 98% Risk" into "Reason: High Velocity + New Device" for the regulator.

13. Glossary of Fraud Terms

- Friendly Fraud: When a legitimate customer makes a purchase and then disputes it ("I didn't buy that!") to get a refund. Hardest for AI to catch.

- Credential Stuffing: Bots trying millions of Username/Password combos stolen from other breaches.

- Busting Out: Using a credit card normally for months to increase the limit, then maxing it out and disappearing.

- Smurfing: Breaking a large money laundering transaction into tiny bits (under $10,000) to avoid reporting thresholds.

- Velocity Check: A rule counting how many times an event happens in a time window (e.g., 5 password resets in 1 min).

Estimate Your Fraud Savings

See how much you could save by reducing fraud losses and manual review time with our interactive calculator.

Frequently Asked Questions

What about "Synthetic Identity" fraud?

This is AI's specialty. Fraudsters combine real SSNs with fake names to build credit over years. AI detects these "Frankenstein IDs" by cross-referencing thousands of third-party data sources that a human would never check.

Does AI help with compliance reporting?

Yes. AI automatically generates Suspicious Activity Reports (SARs) with all the evidence pre-filled, reducing the time to report to FinCEN from hours to minutes.

Is the AI "Black Box" a problem for regulators?

It used to be. Now, we use Explainable AI (XAI). Every fraud decision comes with "Reason Codes" (e.g., "High velocity transactions," "New device"), satisfying regulatory audits.

7. The Threat of Adversarial AI: Hackers Fighting Back

Fraudsters are now using AI to attack your AI. This is an arms race.

Attack Type 1: Poisoning (The Long Con)

- The Tactic: A fraudster feeds "good" data into your system for months (small, verified transactions) to teach your AI that their behavior is safe.

- The Strike: Once the AI trusts them, they execute a massive theft.

- Defense: "Outlier Detection" on training data sets.

Attack Type 2: Model Evasion (The Probe)

- The Tactic: They ping your API million times with slightly different inputs (changing the zip code, then the amount, then the browser).

- The Goal: They reverse-engineer your "Decision Boundary." They find the exact threshold (e.g., "$9,999 is okay, $10,000 is flagged").

- Defense: Rate-limiting API calls and adding "Random Noise" to the decision boundary so it isn't a hard line.

Attack Type 3: Deepfakes vs KYC

- The Tactic: Using a Generative Adversarial Network (GAN) to create a video of a person blinking and nodding to pass a "Liveness Check."

- Defense: Infrared reflection analysis (requires specialized hardware) or "Challenge-Response" (Ask the user to touch their nose).

8. Implementation Roadmap: Deploying Defense

Sprint 1: Data Unification (Month 1)

- Data Lake: Federate data from Cards, Wires, and ACH into a single Feature Store (e.g., Feast).

- Feature Engineering: Create signals like "Device Velocity" (How many logins from this iPhone in 1 hour?).

Sprint 2: Model Training (Month 2)

- Champion/Challenger: Train an XGBoost model (Challenger) and run it against your rules engine (Champion).

- Backtesting: Prove the Challenger catches 30% more fraud.

Sprint 3: The API (Month 3)

- Latency Test: Ensure the model responds in < 30ms.

- Integration: Connect to the Payment Switch (Authorization Stream).

Sprint 4: Policy & Tuning (Month 4)

- Threshold Setting: Decide that Score > 95 is a Block, Score > 75 is 2FA.

- Go Live: Switch traffic to the AI.

9. The Ethical Frontier: Reducing Bias

AI is powerful, but dangerous if unchecked. The Risk: An AI model notices that transactions from a specific zip code have higher fraud rates. It starts blocking everyone from that neighborhood (Digital Redlining). The Solution:

- Fairness Metrics: We optimize for "Equal Opportunity Difference." The False Positive rate must be equal across all demographic groups.

- Protected Class Exclusion: We explicitly remove race, gender, and religion from the training set.

10. The Quantum Threat (Future Proofing)

By 2030, Quantum Computers may break current encryption (RSA). Preparation: Banks must start "Crypto-Agility" planning now, upgrading to Post-Quantum Cryptography (PQC) algorithms to ensure the AI's data remains secure.

Summary

In summary, AI fraud detection is no longer optional for financial institutions facing weaponized deepfakes and synthetic identity rings. By moving from rigid rules to adaptive machine learning and graph analytics, banks can catch 97%+ of attacks while drastically reducing the "insult rate" for legitimate customers.

Recommended Follow-up:

- Financial Services AI Implementation Guide

- Financial Services Regulatory Compliance Guide

- Financial Services Customer Experience

Close the door on fraud: Contact AgenixHub to demo our Real-Time Fraud Prevention engine.

Protect your customers and your reputation. Deploy state-of-the-art AI fraud detection with AgenixHub.